Compelling Opportunities in Industrial Markets on the U.S./Mexico Border

The growth in border industrial demand is occurring alongside heightened uncertainty about U.S. trade policy that is unlikely to fade soon.

While the $1 trillion CLO market has been around for decades, CLO ETFs are fairly new. Previously only available to large institutional investors, the growing CLO ETF market democratizes the investment strategy for retail investors. CLOs have historically provided a combination of attractive spreads, yields, and strong credit profiles. Now, the small but fast-growing CLO ETF segment is garnering increased attention from investors seeking floating rate assets with a strong excess return profile. Actively managed AAA CLO ETFs provide access to the highest-rated tranche in the CLO capital structure, which delivers a sizable yield boost over other fixed income investments of similar credit quality.

However, actively managed ETFs are showing notable dispersion in positioning with some managers more willing than others to reach down in credit quality or move into middle market loans in their search for yield. As a result, not all AAA CLO ETFs are created equally, potentially leading to a wide dispersion in performance—especially during a down-market cycle.

Even as the global monetary tightening cycle appears to be in its last throes, the potential of a higher-for-longer rate environment continues to drive investors’ interest in floating-rate assets. Particularly, retail investors are now just gaining access to the asset class given the advent of CLO ETFs. As such, CLO ETF assets under management have seen a nearly five-fold increase since 2023 to more than $15 billion as institutional and retail investors search for high-quality yield and portfolio diversification.

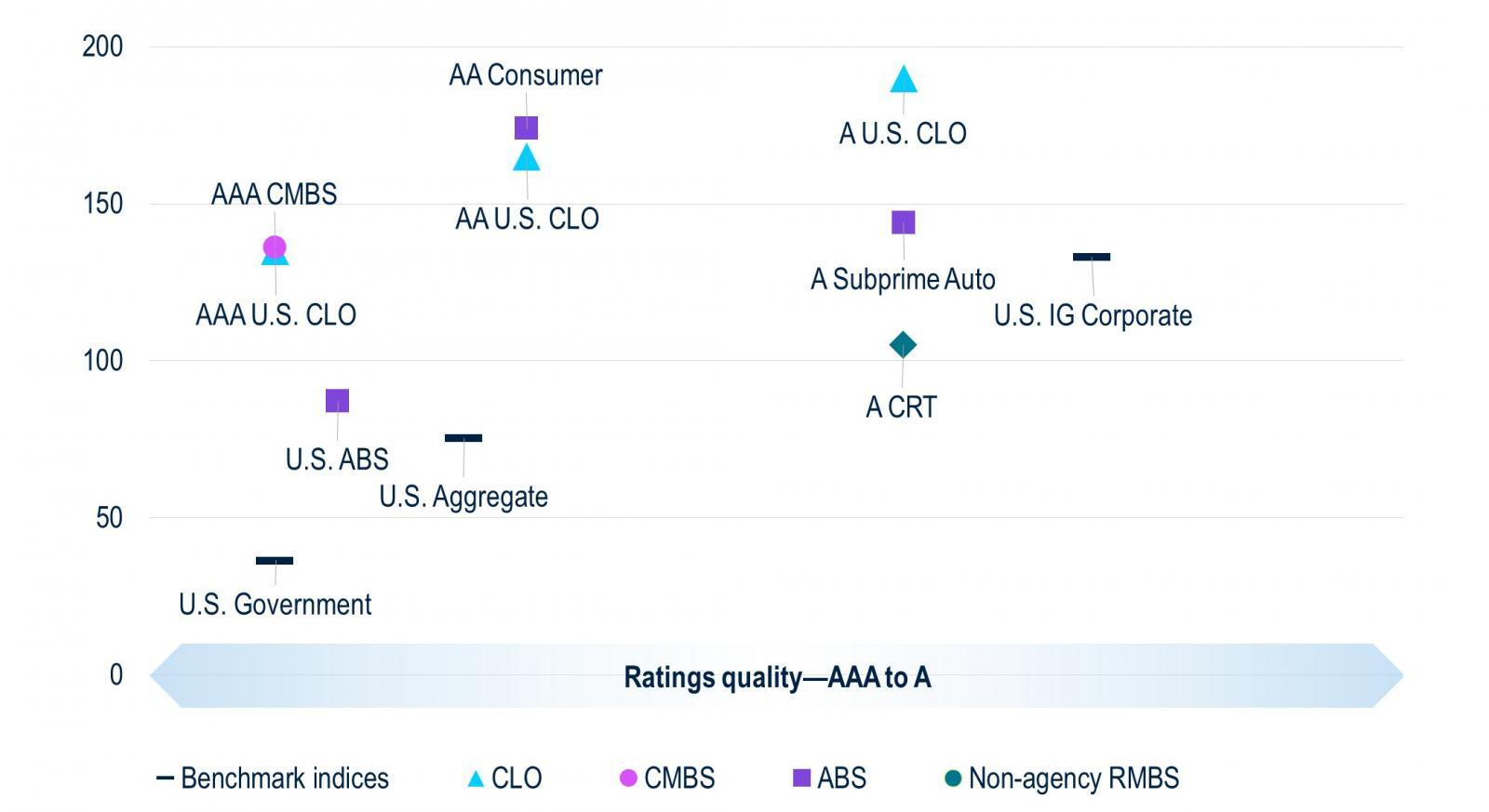

While AAA CLOs, specifically, benefit from strong structural protections and historically low defaults, they also can offer comparatively high yields. When plotted relative to their credit ratings, spreads on high-quality CLOs stand out as they offer some of the highest spreads of any high-grade credit investments (Figure 1).

Source: PGIM Fixed Income as of October 2024.

As a refresher, CLOs are actively managed investment pools of senior secured broadly syndicated loans (BSLs) or middle market leveraged loans. Each CLO is structured as a series of tranches rated from highest to lowest given the percentage of subordination and income stream.

Senior AAA tranches are the most senior, risk remote tranche in the CLO capital structure. The credit enhancement and structural protections of the senior AAA tranches grants them the first claim on cash flows. They also benefit from the credit support of other tranches as realized losses are first absorbed by all tranches subordinate to the senior AAA tranche. In addition to having a priority on cash distributions, AAA tranches have an additional structural enhancement due to performance tests meant to identify and cure any deterioration in the underlying collateral. If tests are tripped, a CLO manager would divert cash flows from equity and then the lowest debt tranches to pay down the senior-most tranches. The combination of strong structural protections and their seniority in the capital structure has resulted in zero AAA losses through their long history.1

Importantly, not all AAAs benefit from being the senior-most tranche. Recently, the market has seen an increasing number of “Junior AAA” tranches. While we believe these tranches are still risk remote, it is important to appreciate that these tranches are not “first-pay” securities and, thus, do not benefit from the amortization protection when triggers are initially tripped. Thus, we observe these securities to behave much more akin to other “second-pay” securities—AA CLOs.

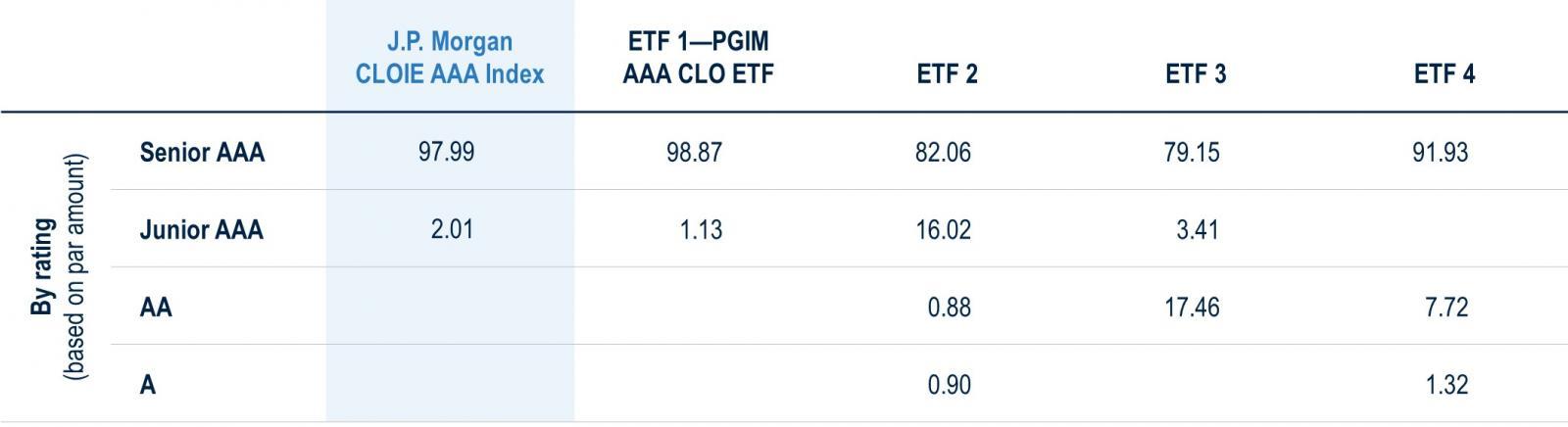

Unlike passive investments that mirror benchmarks, CLO ETFs are all actively managed and differ meaningfully across managers. Even at the AAA space, some managers may choose to reach further down the credit ratings spectrum in exchange for a slight pickup in yield. Others choose to limit the portfolio only to AAA-rated assets. While AAA CLO ETFs may at first appear homogeneous, the composition and credit quality of the underlying portfolios can be vastly different, with junior AAA and even AA tranches comprising a sizeable portion of some portfolios (Figure 2).

Source: JP Morgan, Bloomberg, PGIM Fixed Income as of October 2024. For illustrative purposes only.

CLO ETFs largely fall into one of two buckets—the “AAA” and the “BBB” funds. These broad-brush categories do not necessarily correlate directly to the ratings of the underlying assets. While a CLO ETF may claim to be AAA CLO ETF, some have a higher percentage of non-AAA tranches than others. But nuances exist even within the AAA category, which can be split into “senior” first-pay tranches and “junior” second-pay tranches. Although both receive a AAA rating, the market sensitivity (i.e. beta) and risk-adjusted returns can vary meaningfully. While both are loss remote, “junior” second-pay AAA tranches have been observed to behave more like AA CLOs during times of market stress, such as those experienced during the heights of the COVID crisis.

Even “small” differences in the underlying credit quality of a CLO ETF can have a meaningful impact on the portfolio’s performance—particularly during times of market stress. Given the potential decrease in relative liquidity, we don’t believe investors are adequately being compensated by the marginal pickup in spread offered by “junior” second-pay AAA tranches.

Putting it all together, while SEC 30-day yields across CLO ETFs would suggest portfolio construction is similar, the positioning (Figure 2) shows how different the risk profiles are. Credit curves are very flat, and differences in ETF fees may offset any additional marginal spread from riskier portfolio positioning.

While AAA CLOs may appear homogeneous, credit quality can vary significantly. With some managers more willing to reach down the credit ratings spectrum, increased differentiation across ETFs is likely, with investment managers possessing strong research and credit capabilities best positioned to capture relative value opportunities. This creates the possibility of a wide dispersion of results—especially during times of limited market liquidity or economic stress.

1. S&P Global. (2023, May 26). Default, Transition, and Recovery: 2022 Annual Global Leveraged Loan CLO Default and Rating Transition Study. Accessed November 2024.

A provider of global fixed income solutions.

Visit Website

PGIM’s Best Ideas highlight a host of areas where we believe investors will find promising opportunities.

Learn More

The growth in border industrial demand is occurring alongside heightened uncertainty about U.S. trade policy that is unlikely to fade soon.

A diversified portfolio of sponsored and non-sponsored loans can provide investors with a broader range of deals and potentially better performance over time.

The era of private equity flourishing under low interest rates, followed by a blend of optimism after the COVID-19 pandemic, has shifted.

Today, the revolutionary impact of AI-driven change is becoming evident in most industries and is accelerating.

The maturation of private markets has led to profound change across the global investment landscape.

Investors have historically favored emerging markets for their high growth potential, relative inefficiency and diversification benefits.

Perspectives on portfolio withdrawal rates by integrating spending flexibility and an outcomes metric that better captures the anticipated retiree sentiment.